Debt doesn’t have to define your financial future. Millions of millennials face overwhelming financial burdens, but the right personal finance advice for millennials in debt can turn your situation around. The average millennial carries $117,000 in total debt, with nearly half seeking professional debt counseling services. This crisis affects 67% of millennials who experience anxiety from financial stress, and 49% have suffered panic attacks related to money concerns.

You’re not alone in this struggle. Statistics show that 83% of millennials have delayed major life decisions due to debt, such as buying a home, starting a family, or pursuing further education. In comparison, 66% remain renters instead of homeowners. But here’s the good news: with proven strategies and the right mindset, you can take control of your finances and build a debt-free future.

Understanding Millennial Debt Challenges Today

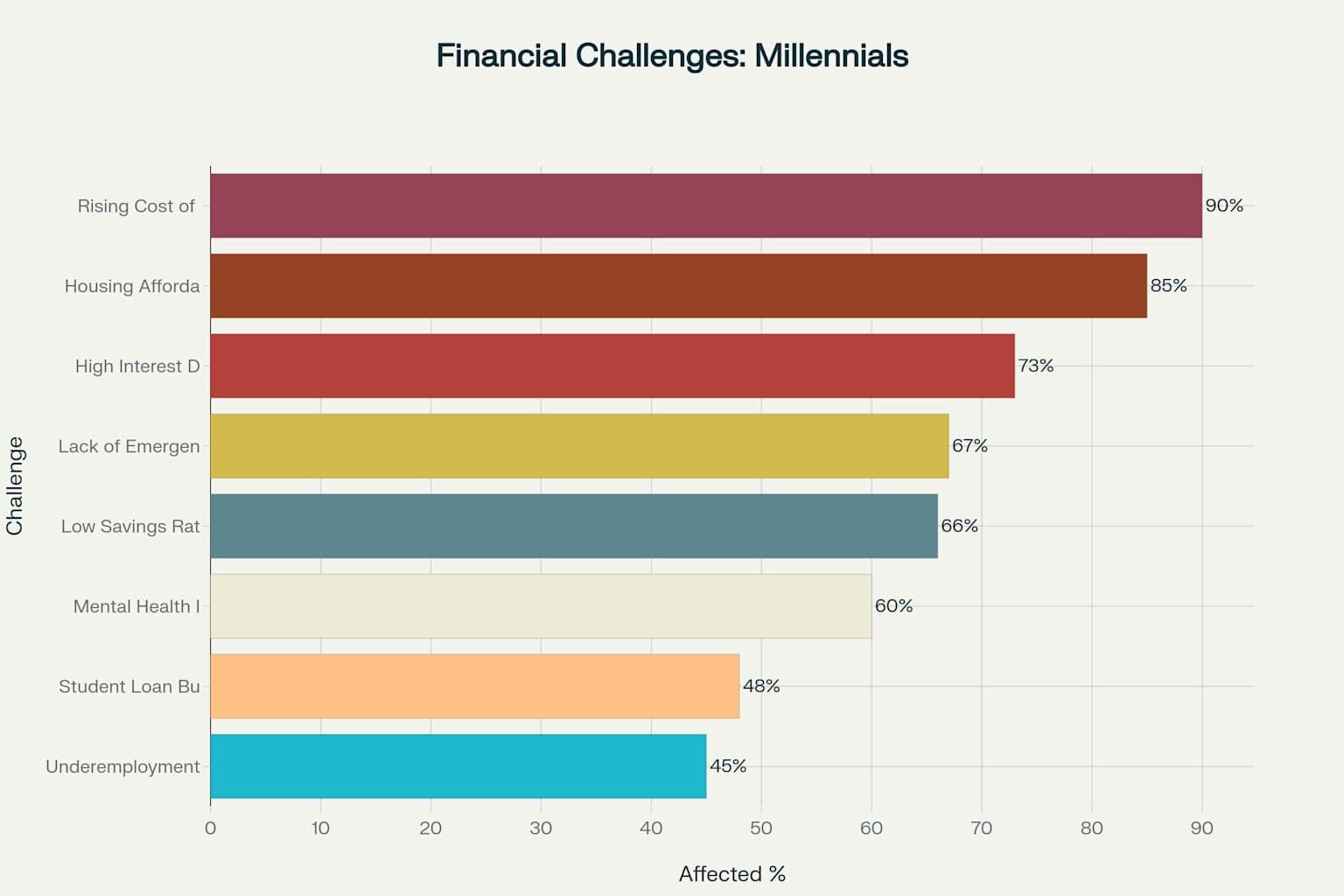

The millennial debt crisis stems from unique economic pressures your generation faces. Student loans average $37,853 per borrower, while credit card debt sits around $6,274. Your non-mortgage debt totals nearly $30,000 on average, creating a debt-to-income ratio of 37.5% for younger millennials. This ratio, which measures your total debt compared to your total income, is a key indicator of your financial health. A lower ratio is generally better, meaning you have less debt than your income.

High inflation and elevated interest rates have made everything more expensive. Housing costs continue rising, making homeownership feel impossible for many. The pandemic disrupted career growth and income stability. These factors create financial stress that affects your wallet and your well-being.

Top Financial Challenges Faced by Millennials by Percentage Affected

Personal finance advice for millennials in debt must address these fundamental challenges. You face higher education costs than previous generations, stagnant wages relative to living expenses, and delayed major milestones like buying homes or starting families. Auto loans now exceed $28,000 in many states, adding another layer of financial pressure.

The mental toll is significant. Financial stress disrupts sleep, decreases energy levels, and impacts relationships. Many millennials avoid dealing with economic issues altogether, making problems worse over time.

Creating Your Debt Repayment Strategy

Choosing a debt repayment strategy is a decisive step towards financial control. Successful debt elimination requires a clear plan tailored to your specific situation. Personal finance advice for millennials in debt starts with understanding exactly what you owe and developing a systematic approach to pay it off.

Assessing Your Complete Debt Picture

Start by listing every debt you carry. Include credit cards, student loans, auto loans, personal loans, and any money borrowed from family or friends. Write down each debt’s balance, minimum payment, and interest rate.

Assessing your complete debt picture may initially feel overwhelming, but it’s a crucial step that can bring a sense of accomplishment. Calculate your total debt load and monthly payment obligations. Many millennials discover they’re paying hundreds of dollars monthly in interest alone.

Don’t forget to include your mortgage if you own a home. While mortgage debt isn’t always “bad debt,” it still affects your overall financial picture and cash flow.

Choosing Between Debt Avalanche and Snowball Methods

Two proven strategies dominate personal finance advice for millennials in debt: the debt avalanche and debt snowball methods. The debt avalanche method first targets your highest interest rate debt, saving you the most money in the long run. The debt snowball method, on the other hand, focuses on your smallest balance first, providing psychological wins that keep you motivated. Each offers distinct advantages depending on your personality and financial situation.

The debt avalanche method targets your highest interest rate debt first. You make minimum payments on all debts, then put every extra dollar toward the debt with the highest interest rate. This approach saves the most money over time by reducing total interest paid.

The debt snowball method focuses on your smallest balance first. You make minimum payments on all debts, then attack the smallest balance with extra fees. Once paid off, you roll that payment amount to the next smallest debt. This method provides psychological wins that keep you motivated.

Choose the method that fits your personality. If you need quick wins to stay motivated, try the snowball approach. If you want to minimize total costs, use the avalanche method. Both work when followed consistently.

Debt Consolidation Options for Millennials

Debt consolidation can simplify your repayment process and reduce interest rates. Personal finance advice for millennials in debt often includes exploring consolidation options that make payments more manageable.

Nonprofit debt consolidation programs offer reduced interest rates of around 8% or lower. These programs combine multiple credit card debts into one monthly payment with counseling support. You’ll pay a small setup fee and monthly service charge, but the interest savings typically outweigh these costs.

Personal loans for debt consolidation work if you have good credit. You borrow enough to pay off multiple high-interest debts, then repay the single loan at a lower rate. This requires discipline to avoid new debt on the paid-off credit cards.

Balance transfer credit cards offer 0% introductory rates for qualified applicants. You transfer existing balances to the new card and pay no interest for 12-21 months. This gives you breathing room to pay down principal, but you must pay off the balance before the promotional rate expires.

Clever Budgeting Techniques for Debt Payoff

Budgeting forms the foundation of practical personal finance advice for millennials in debt. You can’t redirect funds toward debt elimination without knowing where your money goes each month.

Implementing the 50/30/20 Budget Rule

The 50/30/20 rule provides a simple framework for allocating your income. Spend 50% on needs like housing and groceries, 30% on wants like entertainment, and 20% on savings and debt repayment. When carrying significant debt, consider adjusting to 50/10/40 to accelerate payoff.

Track your spending for one month to see where your money currently goes. Many millennials discover they spend more on wants than they realize. Subscription services, dining out, and impulse purchases add up quickly.

Use budgeting apps to automate tracking and stay accountable. Set spending limits for each category and receive alerts when approaching those limits.

Zero-Based Budgeting for Maximum Control

Zero-based budgeting assigns every dollar a specific purpose before you spend it. Your income minus all planned expenses equals zero. This method ensures intentional spending and maximizes funds available for debt repayment.

List your monthly income, then assign amounts to needs, wants, and debt payments. Adjust categories until you’ve allocated every dollar. If you have leftover money, put it toward debt elimination or emergency savings.

Review and adjust your budget monthly. As income and expenses change, your budget should adapt accordingly. This flexibility prevents frustration and keeps you on track.

Technology Tools for Budget Management

Modern budgeting apps make money management easier than ever. Personal finance advice for millennials in debt often emphasizes using technology to stay organized and motivated.

YNAB (You Need A Budget) uses a zero-based approach that assigns every dollar a job. Users report saving an average of $600 in the first two months. The app costs $15 monthly but pays itself through better spending control.

Rocket Money offers comprehensive financial management and bill negotiation services. The app tracks spending, monitors subscriptions, and automatically cancels unused services. Basic features are free, and premium options are available.

PocketGuard specializes in debt payoff planning. The app shows how much you can safely spend after accounting for bills and debt payments. This prevents overspending and keeps your debt elimination plan on track.

Building Emergency Funds While Managing Debt

Personal finance advice for millennials in debt must balance emergency savings with debt repayment. While high-interest debt should be your priority, having some emergency cushion prevents new debt from unexpected expenses.

Starting Small with Starter Emergency Funds

Build a starter emergency fund of $1,000 before aggressively paying down debt. This covers most minor emergencies without jeopardizing your debt elimination plan. The goal isn’t comprehensive coverage but basic protection against life’s surprises.

Save this amount as quickly as possible by cutting expenses, selling items you don’t need, or taking on temporary extra work. Put the money in a separate high-yield savings account that earns interest but remains easily accessible.

Once you’ve eliminated high-interest debt, expand your emergency fund to cover 3-6 months of living expenses. This will protect you against job loss or major financial setbacks.

Strategies for Debt and Emergency Fund Balance

If your situation allows, split the extra money between debt repayment and emergency savings. Put 70% toward debt and 30% toward emergency savings, or adjust the ratio based on your job security and debt interest rates.

Use windfalls strategically. When you receive a tax refund, bonus, or gift money, divide it between debt payoff and emergency savings. This approach maintains progress on both fronts.

Avoid using retirement accounts as emergency funds. Early withdrawal penalties and taxes make this an expensive option. Build separate emergency savings even while carrying debt.

Increasing Income Through Side Hustles

Boosting your income accelerates debt payoff faster than expense cuts alone. Personal finance advice for millennials in debt increasingly includes side hustle strategies that leverage your existing skills and available time.

Popular Side Hustle Options for Millennials

Freelancing offers flexible income opportunities in writing, graphic design, web development, and consulting. Platforms like Upwork and Fiverr connect you with clients needing your skills. Start with competitive rates to build reviews, then increase prices as you gain experience.

Delivery services provide immediate income with flexible scheduling. You can drive for rideshare companies, deliver food through apps like DoorDash, or shop for others through Instacart. These options work around your full-time job schedule.

Online selling generates income from items you already own or products you create. Sell unused belongings on eBay or Facebook Marketplace. Create digital products, handmade crafts, or print-on-demand designs.

Content creation builds long-term income through YouTube channels, podcasts, or social media. While monetization takes time, successful creators earn substantial passive income.

Maximizing Side Hustle Income for Debt Payoff

Set realistic income goals of $1,000 monthly from side work. This amount significantly accelerates debt elimination without overwhelming your schedule. Track your hourly earnings to focus on the most profitable activities.

Treat side hustle income as debt repayment money, not lifestyle upgrade funds. Direct every dollar earned toward your highest-priority debts. This prevents lifestyle inflation from sabotaging your progress.

Consider the tax implications of additional income. To avoid surprises at filing time, set aside 25-30% of side hustle earnings for taxes. Use a separate savings account for tax money.

Balancing Debt Payoff with Future Financial Goals

Personal finance advice for millennials in debt must address the tension between eliminating current obligations and building future wealth. The key is finding the right balance for your specific situation.

Retirement Saving While Carrying Debt

Always contribute enough to your 401(k) to receive the full employer match. This match represents an immediate 100% return on investment, which beats paying off even high-interest debt. The average employer match equals 4.6% of compensation.

For debt with interest rates above 6%, focus on repayment before additional retirement contributions. For lower-rate debt, continue regular retirement savings while making minimum debt payments. This threshold reflects long-term investment return expectations.

Younger millennials benefit most from continued retirement investing due to compound growth over decades. A 25-year-old has 40 years for investments to grow, making even small contributions valuable.

Investment Considerations During Debt Repayment

When deciding priorities, compare debt interest rates with expected investment returns. For example, 20% high-interest credit card debt should be eliminated before investing, while a 4% auto loan might not take precedence over retirement savings.

Consider your risk tolerance and time horizon. Guaranteed debt payoff provides certain returns equal to the interest rate. Investment returns fluctuate and aren’t guaranteed, especially in the short term.

Avoid complex investment strategies while managing debt. Once high-interest debt is eliminated, focus on employer 401(k) matches and basic index fund investing.

Managing Mental Health and Financial Stress

The psychological impact of debt affects your ability to make sound financial decisions. Personal finance advice for millennials in debt must address mental health alongside practical strategies.

Recognizing Signs of Financial Stress

Financial anxiety manifests through sleep problems, decreased energy, relationship conflicts, and avoidance of money-related tasks. Nearly half of millennials experience panic attacks related to finances, while 67% report anxiety from money stress.

Physical symptoms include headaches, digestive issues, and muscle tension. As shame and embarrassment grow, financial stress also impacts work performance and social relationships.

Avoidance behaviors like ignoring bills, avoiding bank account balances, or refusing to discuss money indicate severe financial stress. These patterns worsen debt problems over time.

Stress Management Techniques

Practice mindfulness and meditation to manage anxiety around money. Even 10 minutes daily helps regulate stress responses and improve decision-making abilities. Free apps like Headspace offer guided sessions specifically for financial stress.

Seek support from trusted friends, family members, or support groups. Shame thrives in isolation, but sharing struggles reduces emotional burden and provides accountability. Many communities offer free financial support groups.

If financial stress significantly impacts daily life, consider professional counseling. Mental health professionals can help develop coping strategies and address underlying anxieties about money. Many insurance plans cover mental health services.

Remember that financial problems are often systemic issues, not personal failures. Economic conditions, wage stagnation, and rising costs affect entire generations. Self-compassion helps maintain motivation for positive changes.

The path to financial freedom takes time and persistence, but millions of millennials have successfully eliminated debt and built wealth. Start with one small step today, whether listing your debts, downloading a budgeting app, or researching side hustle opportunities. Your future self will thank you for taking action now.

Personal finance advice for millennials in debt works when you commit to consistent action over time. Choose strategies that fit your personality and situation, then stick with them long enough to see results. You have the tools and knowledge needed to overcome debt and build the financial future you deserve.